Today, we’re going to dig into:

- What blockchain actually is

- How it’s going to affect different industries now and in the future

- 3 core challenges to widespread adoption

- What blockchain means for the internet of things (IoT)

What is Blockchain?

Most people know blockchain as the core technology that enables cryptocurrency, like Bitcoin or Ethereum. But that’s just one application. Blockchain technology extends far beyond cryptocurrencies.

So, what is blockchain tech anyway?

It is a type of distributed ledger technology (DLT), AKA a very large ledger, or data tracking system.

Specifically, blockchain technology allows transactions to be recorded in a way that’s extremely difficult to change once they’ve been added to the blockchain.

Let’s run through an exercise and imagine that the blockchain is as a paper ledger for a small store.

In that ledger, you have money coming in and money going out, every transaction is recorded and public.

This works pretty well. But what if your employee wants to cook the books? They might change how much money comes in or goes out.

But you (the store owner) were super smart and implemented the blockchain method to manage your transactions.

How would this help in case of the untrustworthy employee?

Your store ledger is watched and maintained by everyone who works at your store (in real time), all your employees have a copy of the ledger at all times. As soon as your cheating employee tries to change the data, everyone would say “Hey, that guy’s trying to cook the books. I know because he’s written $20 when I only have $10 recorded!”

This is the miracle that makes blockchain a system that will drive innovation now and in the future. It can drastically reduce the cost of trust by decentralizing our approach to accounting—and, by extension, create a new way to structure economic organizations.

Today, when transactions are processed, they are generally run through a third party approver, usually called a clearing house. They maintain a master record, and control the entry of all data values.

For instance, when you buy something on Amazon, you’re not dealing directly with the person you’re buying from. You’re dealing with a middleman — in this case, Amazon. We do this because without the middleman to enforce standards, rules, and laws, we might trade with our budding fraudster, and we might be ripped off.

Governments, banks, corporations and more all act as middlemen. And this works.

But it’s expensive and can be prone to fraudulent activities.

Amazon, PayPal, banks, credit card providers — they all charge fees associated with trust and the guarantee that when we send our hard-earned cash somewhere, it’s not going to get lost along the way.

So Why is Blockchain Different?

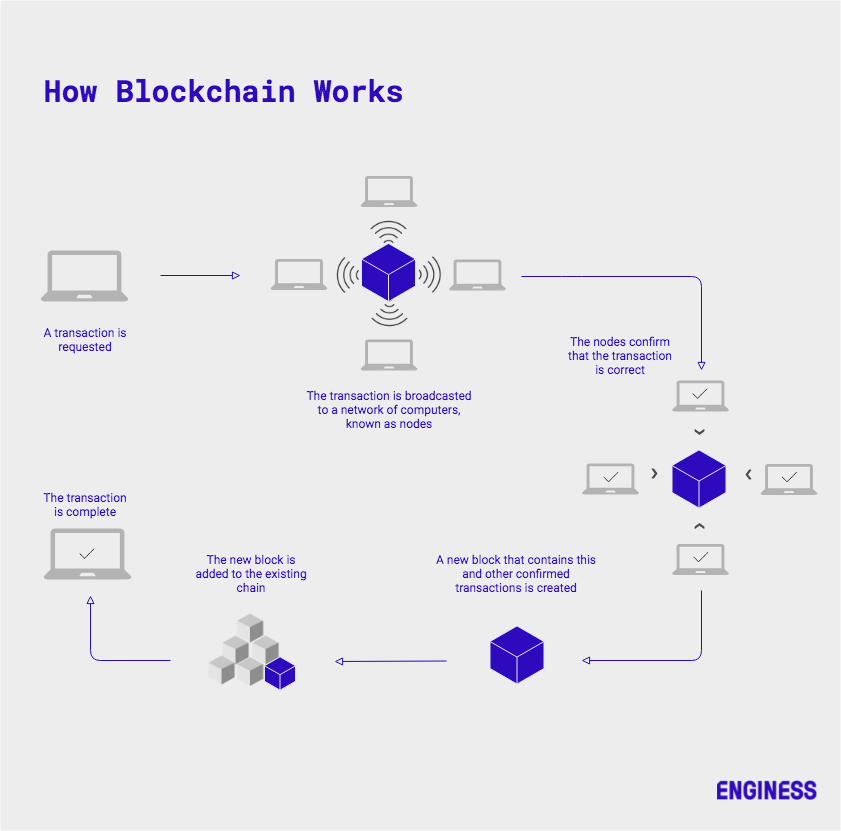

Instead of our ledger being maintained by a single centralized institution, such as a bank or government agency, our digital ledger (in full) is stored on multiple independent computers within a decentralized network. No single entity has ultimate control.

Blockchain achieves this by creating a system where each transaction can only be completed if the distributed network (all the people watching) come to a consensus, and only once this is achieved will all the ledgers be updated.

So, picture our store ledger again. Say you’re entering the new information yourself, having fired your terrible employee.

When you enter a new piece of information, two things happen. First, your transactions get a unique identifier that positions it in the context of all the other transactions that have happened (e.g. transaction B follows transaction A and comes before transaction C).

Next, your new information is recorded in everyone else’s ledger as soon as you write it on your own.

And finally, everyone else gets asked: “Is this right?”

Only when the peer to peer network confirms “yes, this transaction is correct” does your new ledger entry get added and recorded as valid and true, and lumped into a “block” of other transactions that have been verified to be bulk uploaded.

And that, in a nutshell, is what blockchain technology does.

Who Uses Blockchain

Now that we know what we’re dealing with, who is actually using it?

Blockchain technology has been most openly embraced by financial and cryptocurrency markets. The basic pitch is that instead of using a central bank or financial institutions to track transactions, you rely on the P2P network in the blockchain to do that for you. No one can say “Oh, I have a bazillion dollars” because the rest of the network will reject that transaction.

But functionality extends into other industries too. This is where it gets fun: transactions can in principle represent almost anything.

Pharmaceuticals and medical device manufacturers

Regulators increasingly demand constant and perfect tracking of what devices, parts, and pills go where. This gets harder as the volume of data you need to manage grows and the nature of iterative design changes processes and systems.

How you store that data securely and track it as products go to market is incredibly challenging. Blockchain can help by offering a secure and distributed way to guarantee meeting compliance standards while still getting to market quickly.

One example of this is how DHL partnered with Accenture to track pharmaceuticals and devices around the world. As of April this year, the system had 7 billion unique serials in it.

Complex supply chains

Blockchain is all about maintaining data integrity across a wide range of applications.

Global supply chains are continually faced with the challenge of keeping dozens or hundreds of stakeholders up to date in terms of the data they use and updating it as products move through the system. Blockchain can help create a decentralized and accurate data repository without the undue risk of a security breaches. One example of this is Walmart, using blockchain technology to improve their supply chain and optimize tracking. Maersk is also building technology to improve the supply chain via blockchain tech.

Intellectual property (IP) and legal applications

If blockchain creates an undisputed record of who did what and when, then legal applications are a natural fit.

Take IP, for example. Right now, you can file a patent in two different countries and end up mired in an IP legal battle. However, if there was a blockchain-based patent repository, there would never be a conflict over who invented what first.

Now at this point, you might be thinking:

Why are we not all using blockchain for everything?

Turns out, there are some serious challenges still to overcome.

3 Challenges of Blockchain

1. Blockchain is resource hungry

First, every block has to be replicated across every node of a network. That’s a lot of computing power dedicated to network maintenance.

Second, blockchain requires complex hash generation and consensus-seeking scripts for every transaction. This is fine at a small scale, but you look at turning a system like Visa into blockchain, you need to work out a way to process billions of transactions incredibly quickly.

2. Privacy

The nature of blockchain networks is that everyone can see every transaction. And even if every node in the network is anonymous, you can still see what was exchanged and between which wallets. As the applications of blockchain become more diverse, this will present a challenge as transactional data gets shared across the network.

3. Legal battles

Blockchain is set to disrupt a number of legacy industries with powerful lobbying interests. There will be blood. What’s more, blockchain hasn’t had a great start, when its first major public use was via Bitcoin and the infamous dark-web market the Silk Road.

Blockchain also raises powerful arguments around the role of government, corporations, and persistent data and who has a right to it. Data like personal debt, personal information, voting information and more. Now, these are controlled largely by governments. But in the future, that might not be the case.

What This Means for IoT

The dream of the internet of things is simple: every physical product has a sensor in it, passing data back to the network, where it’s aggregated and consumed by AI and machine learning to turn out useful insights.

These insights can guide everything from when a fleet of trucks need their gaskets replaced to when you need to buy more milk.

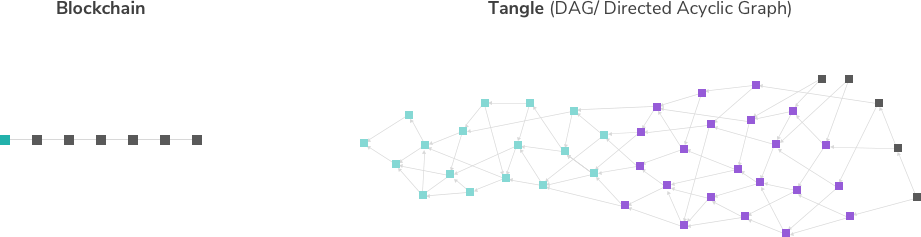

Blockchain enters the picture because it can help solve a few key failings in the IoT ecosystem with a distributed ledger technology called Tangle. Tangle is an open source “permissionless DLT for the modern economy.”

Image Source: IOTA

It’s like a blockchain network. However, instead of transactions being validated by consensus, each transaction only needs to be validated by the two previous transactions.

The way it works is that each node must validate others in order to get a credit to request validation for their own transactions.

Therefore, the only way to make more transactions is to offer more resources to the network, feeding growth and keeping it free and flexible for everyone.

The only real reward is further validation and expansion of the network.

How This Fits Into IoT

Security. Think of a network like a castle — every new connection to it is a new door that will potentially let a threat.

Currently, networks are made-up of computers, phones, and servers, and that’s already a difficult security challenge to maintain.

To see the IoT dream realized, our caste would need 10x the number of doors.

There are serious security repercussions, particularly because humans might not ever see the raw data, meaning that through one door, someone could slip in inaccurate data to trigger potentially disastrous events.

Blockchain and Tangle can provide the much-needed security layer to make the IoT actually functional.

Second, IoT technology is by its nature distributed. This means that it’s time-consuming and difficult to get back to a functional “HQ” quickly enough to be processed and issue accurate commands. Edge computing can mitigate this challenge, but you’re still building on top of a fundamentally different architecture.

Blockchain can help solve this problem since it too is a distributed network. In turn, this makes the IoT more of a reality for enterprise organizations.

Summary

- Blockchain is a distributed ledger system. That means it’s everyone who’s a part of the network has a copy of the blockchain (a list of transactions) and verifies additions to it. This makes it incredibly secure because altering it requires the consensus of the entire network.

- This distributed network lets participants track transactions and data changes on a massive scale without relying on a third party to “oversee” the transactions and store a master copy.

- Blockchain’s functionality is currently overwhelmingly focused on financial transactions. But we’re starting to see expansions into other industries like complex supply chains, pharmaceuticals, manufacturing, a legal / IP applications.

- There are downsides though — blockchain remains relatively obscure in the world of digital transactions, and each one requires an enormous amount of computing power to complete, so there’s a scaling issue. Privacy is an ongoing concern since everyone on the network can see transactions (even if the transactors are anonymous) and legal battles around data function and ownership continue to crop up.

- IoT is great in theory but is running into practical problems around security and network architecture. Blockchain and other distributed ledger technologies can help mitigate those challenges.